The AML Landscape in India: 2025 Edition

Anti-Money Laundering (AML) compliance has moved from a checkbox exercise to a genuine board-level priority for Indian financial institutions. The Financial Intelligence Unit – India (FIU-IND) reported a record number of Suspicious Transaction Reports (STRs) in FY2024, and enforcement actions under the Prevention of Money Laundering Act (PMLA) have surged accordingly.

For businesses operating in banking, insurance, fintech, real estate, and professional services, the question is no longer whether to build AML compliance capabilities — it's how to do it efficiently without creating friction in legitimate customer journeys.

What AML Screening Actually Involves

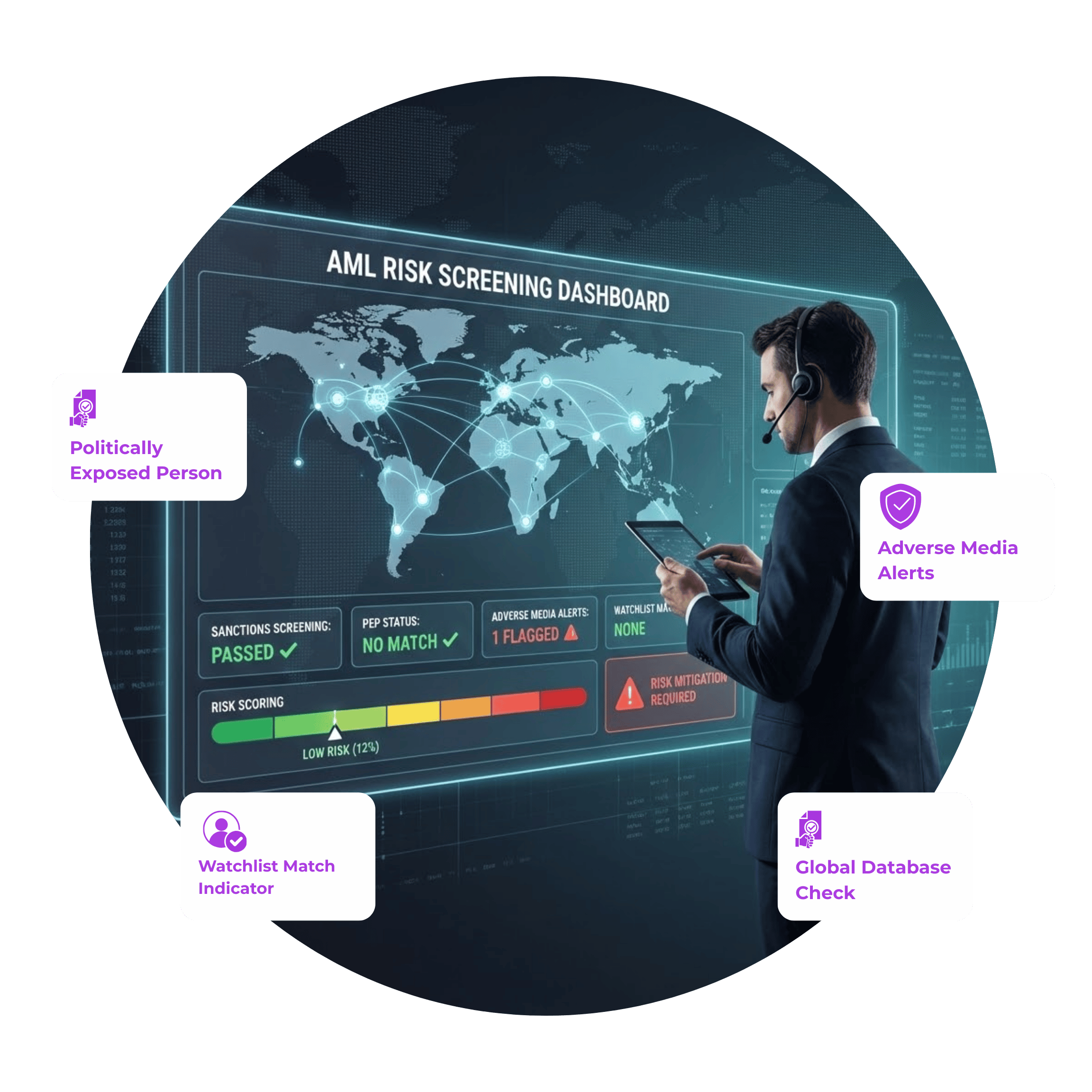

AML screening is the process of checking individuals and entities against:

- PEP lists (Politically Exposed Persons) — Individuals who hold or have held prominent public positions, and their immediate family members and close associates

- Global sanctions lists — OFAC (US), EU, UN, HM Treasury (UK), and India-specific lists

- Adverse media — Structured monitoring of negative news from verified sources

- State-Owned Enterprise (SOE) registries — Entities where a government holds significant ownership

- Indian watchlists — PMLA Schedule lists, ED-designated entities, and RBI caution lists

A thorough AML check doesn't just match a name — it disambiguates matches (many people share common names), scores risk, and builds an audit trail for every decision.

Key Regulatory Updates for 2025

PMLA Amendment — Expanded Predicate Offences

The 2023 PMLA amendments expanded the list of scheduled offences — the underlying crimes whose proceeds can constitute money laundering. Cybercrime, environmental offences, and trafficking-related crimes were added. This means businesses in sectors that previously felt insulated must now re-examine their exposure.

Beneficial Ownership Disclosure

The Companies Act amendments require companies above a certain threshold to disclose Ultimate Beneficial Owners (UBOs) with ≥10% ownership. Financial institutions onboarding corporate clients must now verify UBOs — which means running AML checks on individuals buried behind complex ownership structures.

Digital Lending Guidelines

RBI's digital lending guidelines mandate AML checks for all loan originations above ₹50,000, including Buy Now Pay Later (BNPL) products. Fintechs that previously relied on simplified KYC must now implement full AML workflows.

Building a Compliant AML Workflow

Step 1: Customer Risk Classification

Not all customers carry the same AML risk. Build a Risk Rating Matrix that classifies customers as Low, Medium, or High risk based on:

- Customer type (individual, corporate, PEP, SOE)

- Geographic exposure (high-risk jurisdictions)

- Transaction patterns (cash-intensive business, large transfers)

- Product type (correspondent banking, trade finance, crypto)

High-risk customers require Enhanced Due Diligence (EDD) — including source of funds documentation and senior management approval.

Step 2: Initial Screening at Onboarding

Run a comprehensive AML check at onboarding against all relevant lists. A good screening platform returns:

- A clear match/no-match result with disambiguation

- Risk score and risk factors

- Audit trail with timestamp, data sources, and match rationale

- Periodic re-screening triggers when list updates occur

Step 3: Transaction Monitoring

Onboarding screening is necessary but not sufficient. Real-time transaction monitoring flags:

- Structuring (breaking large transactions into smaller ones)

- Rapid movement of funds (round-tripping)

- High-velocity cash transactions

- Transactions with high-risk counterparties

Step 4: Suspicious Transaction Reporting

When a Suspicious Transaction is identified, your compliance team must file an STR with FIU-IND within the prescribed timeline. A well-designed AML system creates the documentation trail needed to support these filings efficiently.

The Technology Stack for Modern AML

Manual screening is dead. At any meaningful transaction volume, human review cannot keep pace with the speed of digital financial services. The shift is to:

- API-based screening — Real-time checks integrated into onboarding flows

- Fuzzy matching algorithms — To catch name variations, transliterations, and aliases

- Continuous monitoring — Automated re-screening when watchlists update

- Risk orchestration — Routing high-risk cases to human review, auto-approving low-risk

VerifyAll's AML Verification API covers 200+ global sanctions lists, India-specific watchlists, PEP data across 100+ jurisdictions, and adverse media — all in a single API call with a response time under 500ms.

What Non-Compliance Costs

FIU-IND enforcement actions in 2024 included penalties ranging from ₹50 lakh to several crore rupees for AML programme deficiencies. Beyond financial penalties:

- Licence revocation for regulated entities

- Reputational damage from public enforcement actions

- Personal liability for Compliance Officers and Directors in egregious cases

The cost of a robust AML programme is a fraction of these consequences.